Health Insurance Mandate(s) Still in Effect!

The Affordable Care Act’s (ACA) “health insurance mandates” are still in effect, and have most definitely not been abolished. Had the Republican party’s – The American Health Care Act (AHCA) – passed, it would have, among other things, retroactively eliminated both the Individual and Employer mandates. As such, it did not go to a vote, and thus we still have the ACA, and its associated fees, taxes, mandates, regulations, etc.

The ACA requires taxpayers to show that they have minimum essential coverage, which includes but is not limited to Medicare, Medicaid, TRICARE, CHIP, and private health insurance obtained through an employer or the individual market. And, the individual mandate fee still applies to individuals who do not qualify for an exemption (e.g. certain hardships, some life events, health coverage or financial status, and membership in some groups).

For both 2016 and 2017, the individual mandate penalty, if triggered, is calculated two (2) different ways, and affected individuals pay the HIGHER of :

A. Percentage of income

· 2.5% of household income

· Maximum: Total yearly premium for the national average price of a Bronze plan sold through the Marketplace; or

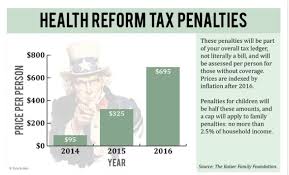

B. Per person

· $695 per adult

· $347.50 per child under 18

· Maximum: $2,085

The federal government (in this case, the IRS) has “relaxed” some of the enforcement of the individual mandate, and associated penalties. Specifically, in February of this year (2017) the IRS stated that, starting this tax season, it will no longer systematically reject returns on which the taxpayer doesn’t indicate their coverage status. However, the agency may still follow up with questions directed to filers.

So unless and until there is a change in regulations, policy, and/or law, the individual mandate is the law of the land, and affected individuals are encouraged to comply.

#####